.svg)

Resources

.png)

Addressing Post-Settlement Disputes Efficiently with QSFs

Eastern Point Trust Company Unveils Comprehensive Guide on Navigating Post-Settlement Disputes and Complexities with Qualified Settlement Funds

[5/17/2024] — Eastern Point Trust Company is pleased to announce the release of a new guide designed to address the challenging intricacies of post-settlement litigation disputes. The guide focuses on utilizing Qualified Settlement Funds (QSFs), also known as 468B trusts, as a streamlined solution for efficient settlement fund management and dispute resolution.

It is not uncommon for secondary disputes to arise following a litigation settlement or court award. These disputes can range from family disagreements over their "fair share" to lawyers disputing fee splits, plaintiffs contesting attorney fees, and third-party lien holders emerging to stake claims against the litigation proceeds. Such complexities often hinder the settlement process and prolong the resolution.

Eastern Point Trust Company's newly released guide provides detailed insights into how QSFs can be employed to manage these disputes effectively. By offering a structured approach to fund management and tax compliance and providing the necessary time for informed decision-making, QSFs present a viable solution to post-settlement challenges.

Sam Kott, Vice President of Eastern Point Trust Company, emphasized the significance of the guide, stating, "This guide explores the advantages of QSFs, specifically their ability to address complex issues such as post-settlement disputes, secondary litigation, and lien resolution. The guide also provides direction on navigating post-settlement challenges and highlights the benefits of QSFs in achieving the best possible outcomes for all parties involved."

The guide delves into the various advantages of utilizing QSFs, including:

- Efficient Fund Management: QSFs ensure that settlement funds are FDIC-insured, reduce misallocation risks, and ensure fair distribution.

- Tax Compliance: QSFs help maintain compliance with tax regulations, thereby minimizing potential tax liabilities for the parties involved.

- Informed Decision-Making: By providing time and space for thoughtful decision-making, QSFs help to resolve disputes amicably and equitably.

Eastern Point Trust Company invites legal professionals, plaintiffs, and all interested parties to explore the guide and discover the transformative potential of QSFs in post-settlement dispute resolution. To read the complete guide and learn more about the advantages of QSFs, visit here.

PRESS Contact

www.EasternPointTrust.com

info@easternpointtrust.com

Phone: 855-222-7513

Advantages of Qualified Settlement Funds vs. Environmental Remediation Trusts

Overview

From time to time, Eastern Point Trust Company (EPTC) receives requests to create and administer a Qualified Settlement Fund (“QSF”) pursuant to 26 CFR §1.468B-1 et. seq to fund current or future liabilities (by way of example, future response or remediation requirements) arising from Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”) claims (and violations of state and local environmental law).

This White Paper summarizes via a FAQ format the utilization of a QSF established and operated pursuant to 26 CFR §1.468B-1 related to funding CERCLA environmental claims (and violations of state and local environmental law) and the key advantages of a QSF over an Environmental Remediation Trust (“ERT”) established under IRC §301.7701.

The author assumes for this paper that the reader is familiar with CERLA, ERTs, the associated federal, state, and local environmental law, and the related environmental remediation liability aspects and processes.

Questions and Answers

1. What are the requirements for a QSF?

Answer: On December 23, 1993, the IRS issued a final regulation regarding Qualified Settlement Funds, which went into effect on January 1 as 26 CFR §1.468B-1 et seq., establishing the qualification and operational requirements for a QSF.

26 CFR §1.468B-1 included torts, breach of contract, violation of law, and environmental claims under CERLA as qualifying events.

According to 26 CFR §1.468B-1(c), a QSF must meet the following criteria:

“(c) Requirements. A fund, account, or trust satisfies the requirements of this paragraph (c) if -

(1) It is established pursuant to an order of, or is approved by, the United States, any state (including the District of Columbia), territory, possession, or political subdivision thereof, or any agency or instrumentality (including a court of law) of any of the foregoing and is subject to the continuing jurisdiction of that governmental authority;

(2) It is established to resolve or satisfy one or more contested or uncontested claims that have resulted or may result from an event (or related series of events) that has occurred and that has given rise to at least one claim asserting liability -

(i) Under the Comprehensive Environmental Response, Compensation and Liability Act of 1980 (hereinafter referred to as CERCLA), as amended, 42 USC 9601 et seq.; or

(ii) Arising out of a tort, breach of contract, or violation of law; or

(iii) Designated by the Commissioner in a revenue ruling or revenue procedure; and

(3) The fund, account, or trust is a trust under applicable state law, or its assets are otherwise segregated from other assets of the transferor (and related persons).”

2. Does a QSF qualify for use to fund the associated liabilities under CERCLA (e.g., future response or remediation requirements)?

Answer: Yes, a QSF, pursuant to 26 CFR §1.468B-1(c)(2)(i), qualifies to fund the associated liabilities under CERCLA if:

“it is established to “resolve or satisfy one or more contested or uncontested claims that have resulted or may result from an event (or related series of events) that has occurred and that has given rise to at least one claim asserting liability -

(i) Under the Comprehensive Environmental Response, Compensation and Liability Act of 1980 (hereinafter referred to as CERCLA), as amended, 42 USC 9601 et seq.

(ii) Arising out of a tort, breach of contract, or violation of law; or”…

As noted, 26 CFR §1.468B-1(c)(2)(i) implicitly provides for liabilities under CERCLA as eligible for QSF treatment if (pursuant 26 CFR §1.468B-1(f)(2)) the transferor’s sole remaining liability to the Environmental Protection Agency (“EPA”) upon transfer to the QSF “is a remote, future obligation to provide services or property.”

“(2) CERCLA liabilities. A transferor’s liability under CERCLA to provide services or property is described in paragraph (c)(2) of this section if following its transfer to a fund, account, or trust the transferor’s only remaining liability to the Environmental Protection Agency (if any) is a remote, future obligation to provide services or property.”

Notwithstanding the foregoing, and pursuant to 26 CFR §1.468b-1(c)(2), if, on a facts and circumstances basis, a QSF established in good faith on the then known facts would remain qualified if reopener claims arose as new claims arising from “claims that have resulted or may result from an event (or related series of events).”

Practice Note: It is common to have multiple QSFs associated with the same event. Nothing in 26 CFR §1.468B-1 et seq. prohibits the bifurcation of liabilities into multiple QSFs, each addressing different elements of the claims, different transferors, or other administrative-related segmentation. However, a QSF may not hold claims arising from an unrelated series of events.

Practice Note: As clarified in 26 CFR §1.468B-1 - Example 7 (regarding a landfill operator), there must be at least one claim asserting a liability. General business obligations are not a claim, such as a future cost to perform, even if the law nominally requires the obligation.

PLR Number: 200821019 Release Date: 5/23/2008 clarifies that the funds in the QSF must “resolve or satisfy claims described in section 1.468B-1(c)(2)” and Example 7 considered the following scenario: “There a corporation owned and operated a landfill in a state that required the corporation to transfer money to a trust annually based on the total tonnage of material placed in the landfill during the year. Under the law, the corporation is required to perform (either itself or through contractors) specified closure activities when the landfill is full, and the trust assets would be used to reimburse the corporation for these closure costs. The trust in that example is not a qualified settlement fund because it is established to secure the liability of the corporation to perform such closure activities.”

Additionally, 26 CFR §1.468B-1(c)(2)(ii) provides that claims “Arising out of a tort, breach of contract, or violation of law” qualify under the regulation. Thus, those liabilities arising from violations of state law and other environmental laws comparable to the federal CERCLA, to the extent they satisfy 26 CFR §1.468B-1(c)(2)(ii), qualify for transfer into a QSF.

Practice Note: QSFs have unique qualifications and operational requirements; the best practice is to have an independent, institutional trustee with well-established experience appointed to administer a QSF and act as the trustee. The trustee shall act on behalf of the QSF, established as a trust under state law, to enter into a Settlement Agreement between the QSF and the EPA (or other applicable state agency). The associated Settlement Agreement, incorporated into the terms of the QSF, formalizes the agreement between the trustee acting on behalf of a QSF and EPA (or other applicable state agency), defining the obligations under the QSF.

3. Does a QSF provide tax advantages over Environmental Remediation Trusts?

Answer: Yes, unlike ERTs, which provide for no Economic Performance at the time of funding, a QSF pursuant to 26 CFR 26IRC §1.468B-3(c)(1) provides for the “Economic Performance” of the “transferor” at the time of the irrevocable funding of the QSF. Accordingly, a QSF, which is properly qualified, allows a current-year tax deduction of the irrevocable funding amount(s).i

“In general. Except as otherwise provided in this paragraph (c), for purposes of section 461(h), economic performance occurs with respect to a liability described in 26 CFR §1.468B-1(c)(2) (determined with regard to 26 CFR §1.468b-1(f) and (g)) to the extent the transferor makes a transfer to a qualified settlement fund to resolve or satisfy the liability.”

By contrast, an ERT is a Grantor Trust, and each respected funder of an ERT is a “Grantor,” which retains ownership and control of the funds in the ERT, for tax purposes, and the Grantor Trust rules apply. Under the Grantor Trust rules, the funder of an ERT is the owner of the portion of the ERT contributed by that respective Grantor, as the funding does not constitute Economic Performance. Only when the ERT makes payments for the remediation project are the corresponding amounts deductible by the Grantor(s), and only in the current tax year in which the payments occur.

As such, the Grantor is not allowed to claim a deduction based solely upon the funding of the ERT.

4. May existing funds within an ERT be transferred into a QSF, and correspondingly, the transferor allowed a tax deduction at the time of the transfer?

Answer: Yes, funding transferred from an existing ERT into QSF would constitute Economic Performance and allow the “transferor” a corresponding tax deduction for the funding amount in the current tax year.

5. Does a QSF allow for installment or multiple funding by the transferor, and will the funding of a QSF be eligible for a current-year tax deduction?

Answer: Yes, 26 CFR §1.468B-1 et seq. establishes no limit on the number of funding events within the lifetime of a QSF, and each funding of a QSF shall constitute Economic Performance at the time of funding. The deduction of multiple fundings within the current year tax is likewise afforded to the transferor.

6. Environment remediation can take decades; is there a maximum duration for a QSF?

Answer: No, there is no statutory or regulatory time limit on the duration of a QSF. A QSF may operate for so long as potential liabilities are outstanding.

7. Once funded, are the assets/value of a QSF or the associated environmental remediation liability carried on the transferor’s Balance Sheet?

Answer: No, unlike an ERT, upon establishing a QSF, the transferor irrevocably transfers the funding and the associated value of the liability to the QSF. Therefore, the transferor no longer carries on their Balance Sheet the transferred portion of the environmental remediation liability or the assets held within the QSF.

Practice Note: Transferors report that the ability to remove liabilities from their Balance Sheet irrevocably provides secondary benefits of isolating liabilities and improving their reportable financial condition.

8. Does the transferor recognize the realized investment gains, interest, and dividends within a QSF as reportable income?

Answer: No, unlike an ERT (whose assets and investment gains are the transferor’s property), a QSF is responsible for its tax liability and files its own IRS Form 1120-SF (https://www.irs.gov/pub/irs-pdf/f1120sf.pdf).

Accordingly, a QSF is a separate entity, and the transferor has no ongoing accounting, tax liability, or reporting requirements related to the operation of a QSF.

Pursuant to 26 CFR §1.468B-2, a QSF is subject to taxation on its modified gross income. A QSF must file IRS form 1120-SF each tax year it exists (even if it has no assets) until terminated. The trustee/administrator of a QSF typically prepares and files the IRS Form 1120-SF along with any necessary 1099 reporting requirements that may arise from distributions made during the operation of a QSF.

Practice Note: A QSF’s tax treatment of income, distributions, deductions, and income differs materially from the rules generally governing trust taxation via IRS Form 1041. Seek the advice of an experienced QSF tax professional.

9. May excess funds in a QSF be returned to the transferor and preserve the original funding deduction?

Answer: No, if excess funds remain in a QSF upon satisfying all environmental remediation obligations and claims and the pending termination of a QSF, there is no option to revert the funds to the transferor without compromising the transferor’s original deduction of the funding. Reverting the funds to the transferor would nullify the deductibility of the original transfer in the year of funding, thereby necessitating the transferor to file an amended tax return(s) for the year(s) corresponding to the original deduction(s).

Excess funds may offset trustee/administrator expenses, tax liabilities of the QSF, accounting and legal services of the QSF, notification of claimants and claim processing expenses, or other deductions.

Practice Note: One should be conservative in funding a future liability as additional funding may be added to the QSF at any time, but generally, excess funds may not revert without impacting the qualification of the QSF (some exceptions may apply as noted in PLR Number: 200821019 Release Date: 5/23/2008). If excess funds exist, it is not uncommon for a QSF to make a charitable contribution to distribute them or transfer / escheat them to an appropriate government entity.

10. Is the transferor required to fund the entire liability into a QSF, and must the funding occur in a single funding instance or tax year?

Answer: No, a transferor may choose to fund all or any portion of the potential or actual liability for environmental remediation, into a QSF, at their discretion. The corresponding liabilities are transferred into a QSF, and Economic Performance occurs as the funding occurs.

Practice Note: When applicable, transferors have conducted studies to determine the Net Present Value of funding required to offset the liabilities. Utilizing actuarial studies and or an appropriate funding vehicle, the transferor funds the associated QSF with the Net Present Value of the liabilities. In such a circumstance, transferors have transferred the entire liability to the associated QSF. However, the transferor may only claim a tax deduction for the actual funding, not the future value of the entire transferred liability. Further, depending on the investment performance of the assets within a QSF, additional funding into a QSF may be required to fulfill the potential or actual liability for environmental remediation liabilities if they exceed the associated QSF’s available funds. A fixed-income investment vehicle such as an annuity can pre-fund and match the long-term stewardship obligations. With an appropriate inflation factor, some cleanup companies shall agree to a guaranteed fixed-price contract. (The details of such arrangements are not within this White Paper’s scope.)

11. Must a court order or approve a QSF?

Answer: No, pursuant to 26 CFR §1.468B-1(c)(1), a QSF must meet the following criteria regarding governmental approval:

“(c) Requirements. A fund, account, or trust satisfies the requirements of this paragraph (c) if -

(1) It is established pursuant to an order of, or is approved by, the United States, any state (including the District of Columbia), territory, possession, or political subdivision thereof, or any agency or instrumentality (including a court of law) of any of the foregoing and is subject to the continuing jurisdiction of that governmental authority;”

Eastern Point’s online turnkey QSF platform allows you to design a QSF in as quickly as 15 minutes and create a QSF in as little as a single day, including the necessary governmental authority approvals and the IRS granting an EIN.

12. May a transferor also transfer property, such as real estate, to fund a QSF?

Answer: Yes, pursuant to 26 CFR §1.468B-1(d), a transferor may transfer (fund) “money or property to a qualified settlement fund to resolve or satisfy claims”

“Definitions. For purposes of this section -

(1) Transferor. A “transferor” is a person that transfers (or on behalf of whom an insurer or other person transfers) money or property to a qualified settlement fund to resolve or satisfy claims described in paragraph (c)(2) of this section against that person.”

Property such as real estate may be contributed to a QSF to fund claims settlement, but not as an income-producing property. IRS regulations prescribe the method to value property transfers to a QSF properly. The initial basis for the property a QSF receives is the property’s fair market value on the date of transfer to the fund.

Practice Note: Exercise caution to ensure a fair market valuation of the transferred property, which establishes the property’s initial basis.

Summary

QSFs provide material tax and financial advantages over an ERT.

QSF Advantages:

- Funding the QSF constitutes Economic Performance, allowing the transferor to accelerate a tax deduction of funds transferred into the QSF in the current tax year of the transfer.ii

- For financial reporting and tax purposes, a QSF is off balance sheet as both the transferor’s liability and the associated funding transfer irrevocably to the QSF.

- QSFs can facilitate settlement agreements to capitate and settle the environmental liability of the transferor, releasing the transferor.

- QSFs can be easily established and assure regulators and interested parties that funds are irrevocably available to ameliorate environmental liabilities.

- QSF eliminates future administrative burdens associated with an ERT as the trustee assumes the QSF’s administration.

- If a corresponding settlement agreement applies, the QSF assumes the environmental liability from present and any future claims under CERCLA, state, and local law.

Today’s QSF industry provides quick, inexpensive, and easy solutions to implement a QSF to fund environmental remediation liabilities with material tax and financial advantages.

ABOUT EASTERN POINT TRUST COMPANY

Eastern Point Trust Company is a global leader in trust innovation, providing technology-empowered services to individuals, courts, and institutional clients around the world.

Eastern Point is the only “end-to-end” turnkey QSF escrow solution., As an experienced provider, Eastern Point allows for QSF creation, approval, and operation in as little as one business day for QSF of all types.

How the Plaintiff Recovery Trust Can Help E. Jean Carroll and Others

After the plaintiff double tax reduces her settlement, E. Jean Carroll may find herself shopping at Walmart.

As you may know, E. Jean Carroll was recently awarded $83 million in her defamation case against former President Donald J. Trump. After the case Ms. Carroll quipped to Rachel Maddow on MSNBC, “I have such great ideas for all the good I'm going to do with this money”.

“First thing Rachel, you and I are going to go shopping at Bergdorf’s.”

But wait, there is the double tax bite. As all of Ms. Carroll's settlement proceeds are taxable, It is therefore subject to the plaintiff's “double tax” under the Supreme Court's banks taxation ruling. Thus, if her attorney receives a typical 40% contingency fee, then, of the $83 million, she will only end up with approximately $7.5 million; just nine cents on the dollar. Even if her award is reduced on appeal, the same double taxation treatment applies.

The good news is that the Plaintiff Recovery Trust, sponsored by Eastern Point Trust Company and Forward Giving, can eliminate the double tax burden. It does so by eliminating the plaintiff's requirement to pay tax on the attorney fee portion of the settlement, thereby materially increasing the plaintiff's net after-tax proceeds.

Contact Eastern Point to learn how the Plaintiff Recovery Trust may increase your after tax recovery up to 150%.

.png)

Why Qualified Settlement Funds Are a Valuable Tax and Financial Planning Tool in Personal Injury Cases

When confronted with resolving a personal injury case, whether or not involving a client reliant on public assistance, intricate issues such as the allocation of proceeds, settlement planning, and lien negotiations must be meticulously managed. One critical question arises: where can the settlement funds be temporarily held while establishing any requisite public benefit preservation trusts, determining the distribution of proceeds, devising a comprehensive financial plan, and finalizing lien negotiations? How can one secure immediate payment from the defendant without compromising the client’s potential settlement planning strategies?

The solution to these complex challenges lies in utilizing a Qualified Settlement Fund (QSF), also known as a 468B Trust. Continue reading to gain a deeper insight into QSFs and understand why they are essential for personal injury attorneys to master.

What Is a QSF

A Qualified Settlement Fund is a provisional trust (think of it as “tax limbo”) established to manage the settlement funds received from one or more defendants. The primary function of a QSF is to distribute the deposited funds to multiple claimants pursuant to the parties’ agreement or, if necessary, a court order. The QSF termination occurs once all the funds are vested and distributed.

There are several benefits to utilizing a QSF in complex settlements. Chief among them is the simplicity of its establishment. There are only three stipulations for forming a QSF. First, the QSF has approval requirements from a “governmental authority” with jurisdiction over the QSF. Second, the QSF must settle only tort claims or other legal disputes as outlined by Treasury regulations 1.468B-1, et seq. Finally, if established as a trust, it must qualify as such under relevant state law. Any “governmental authority,” irrespective of its jurisdiction over the case, can approve the establishment of the QSF and maintain continuing oversight of the QSF.

Qualified Settlement Funds are a provisional repository for litigation and settlement proceeds. Its purpose is not to function as a perpetual support trust for claimants. Instead, the QSF remains operative only until all allocation disputes among parties and third-party liens are complete and the necessary planning for fund distribution is final. This duration can sometimes extend from several weeks to months or even years.

PRO TIP: No predefined time constraint exists on how long a QSF can remain active. Using a QSF to serve as a long-term tax deferral vehicle is improper. The best practice is that a QSF should remain open no more than 12 calendar months beyond resolving all secondary issues and disputes.

QSFs provide numerous advantages for all involved parties, particularly concerning tax implications, income timing, and settlement planning requirements. A QSF allows for establishing a tax-exempt structured settlement and a tax-deferred arrangement for attorney fees. The management of income timing is possible with a QSF. Generally, claimants are not taxed on the amounts held within the QSF until those amounts are vested by the trustee and disbursed. Additionally, a QSF affords claimants additional time and flexibility (through tax deferral) to make informed decisions regarding their tax, financial planning, and settlement planning strategies.

Benefits of a Qualified Settlement Fund

The benefits for a defendant are that transferring the associated proceeds into the QSF results in an immediate tax deduction in exchange for their permanent release from the obligation. This benefit is significant for defendants, who usually cannot claim a deduction until the claimant receives the funds, which can be postponed in complex settlements.

PRO TIP: Note that the timing of distributions to the claimants from the QSF does not affect the defendant’s ability to claim this tax deduction concurrently upon the transfer.

For the plaintiff, the benefits are the advantage of unrushed additional time to explore tax and financial planning options and resolve liens and other types of secondary disputes. This benefit is significant for plaintiffs, as valuable tax and financial options would otherwise not be available.

QSF Structure

The tax structure for Qualified Settlement Funds is straightforward. Each QSF is assigned a unique Employer Identification Number (EIN) by the Internal Revenue Service. QSFs are subject to taxation based on their modified gross income, excluding the monetary settlement or award receipts, and the corporate income tax rate applies only to the “investment income” of the QSF. Consequently, the tax obligation pertains to the growth of the principal amount through interest or dividends minus permissible deductions such as administrative expenses.

Internal Revenue Code §468B, alongside the Income Tax Regulations articulated in §1.468B-1, et seq., governs the application of a Qualified Settlement Fund. These statutes stipulate that a defendant may execute a qualifying payment to the QSF, thereby achieving “economic performance” — a critical tax consideration for the defendant. Consequently, the trustee of the QSF is empowered to accept settlement funds, enabling the defendant to claim a deduction for the current fiscal year and extricate themselves from litigation.

Post receipt of the settlement/litigation proceeds, the QSF trustee can consent to future periodic payments to a plaintiff, delegate this responsibility to a third entity by assignment or novation, and facilitate the plaintiff’s reception of tax-exempt payments under Internal Revenue Code §104(a) coupled with §130. This specific provision excludes structured settlement periodic payments from being counted as gross income in personal injury cases.

PRO TIP: If the settlement is paid into the law firm’s IOLTA, the plaintiff loses the ability to assign, novate, or structure. Likewise, the same loss of ability to enter into an attorney fee structure or assign occurs when funds are received into the IOLTA.

The Process of Utilizing a QSF

Establishing a QSF is a straightforward process in terms of procedural steps. Initially, the “governmental authority” is petitioned to form the QSF. The governmental authority receives the associated petition and documents and approves the establishment of the QSF. Upon the court’s approval and signing of the order, the defendant(s) issue the payment(s) to the QSF by wire or a check, and in exchange, the associated defendant receives a release from liability pertaining to the payment.

PRO TIP: A QSF’s records should document the payment into the QSF rather than directly to the plaintiff or the law firm.

The timing of distributions from a QSF is contingent upon either an agreement with the plaintiffs or an order by a court. When disbursing funds from the QSF, it is incumbent upon the trustee to secure a release from the claimants (or their agent), which serves as evidence that their claims against the QSF have been resolved or satisfied by the distribution. Upon the disbursement of all funds, the trustee terminates the QSF.

QSFs Mitigate the Settlement Time Pressure

QSFs are an essential resource for personal injury trial attorneys primarily because they speed up the process by mitigating the time pressures associated with lien negotiations, allocations, and probate processes.

The conclusion (whether by settlement or award) of a personal injury lawsuit often leads to a frenzied period to finalize details, a situation referred to as the “settlement pressure cooker.” In such hurried circumstances, one might overlook critical details, neglect vital settlement planning matters, trigger unnecessary accelerated taxation, or unfairly pressure the plaintiff to make hasty decisions.

Establishing a QSF enables the receipt of settlement funds, allowing sufficient time for meticulous future planning.

PRO TIP: Plaintiff counsel can promptly receive payment of the claimant’s attorney fees and costs obligations while allowing the plaintiff’s portion net of the plaintiff’s attorney fee obligations to remain in the QSF.

PRO TIP: The QSF is the sole owner of the funds and the associated income of the QSF (§468B(b)(c)(3)). Until the trustee vests a benefit, no claimant has any vested right. Further, the claimants may have a personal obligation to their attorneys for a portion of the settlement as fees, but that obligation vests no rights to the attorneys within the QSF. Therefore, attorneys have no greater standing than any other party that may have a general personal lien against a claimant. Thus, when the QSF makes payments to the attorneys, such payment is solely from the claimant’s proceeds for the administrative convenience of the claimant to fulfill the claimant’s personal obligation.

Once the defendant transfers “collected” funds into the QSF, the claimant may “petition the trustee” to vest and disburse funds subject to all other factors, such as allocation, the satisfaction of liens, resolution of secondary disputes, etc. This arrangement facilitates the negotiation of liens, determining fund allocations, implementing public benefit preservation trusts, and considering settlement planning issues, including structured settlements. Moreover, this mechanism preserves the attorney’s ability to assign or structure their fees. Consequently, the QSF is a valuable tool for trial attorneys to implement effective financial planning.

Conclusion

QSFs serve as a unique tool and valuable resource in personal injury cases by removing the post-settlement/litigation time pressures and affording flexible tax and financial planning options for the defendants, the plaintiffs, and the plaintiff lawyers, as well as facilitating lien resolution and the option to deal with post-settlement secondary disputes.

What to Do When Family Members (And Even the Lawyers) Are Fighting Over the Settlement Proceeds

Navigating Post-Settlement Complexities with a Qualified Settlement Fund

Great! You have won the case but now face secondary claims and litigation.

No, you are not the first to encounter these issues, and it is not uncommon for post-settlement secondary disputes to occur. For example, families argue over their “Fair Share,” lawyers dispute fee splits, plaintiffs dispute attorney fees, 3rd party lien holders come out of the woodwork to make claims against the litigation proceeds, and more.

Navigating the post-settlement challenges can be overwhelming for lawyers and their clients. But, there is a simple solution - a Qualified Settlement Fund, also referred to as a 468B trust, presents an option to simplify the post-settlement process and handle the hurdles that emerge. By setting up a QSF, the parties can resolve the secondary issues, effectively preserve the settlement funds, ensure tax compliance, and allow time for making informed decisions by deferring taxation.

Here, we delve into the details of QSF and its valuable role in post-settlement planning and administration.

Understanding Qualified Settlement Funds (QSFs)

A Qualified Settlement Fund, sometimes shorthanded as a “QSF,” is an entity created according to IRC Section 468B and its associated regulations to settle various legal disputes. Defendants can place funds into a QSF and receive a release from liability while allowing time for the other parties to resolve secondary disputes and carefully consider their settlement proceeds options.

QSFs trace back to the Tax Reform Act of 1986, which incorporated Section 468B into the Internal Revenue Code. Initially utilized in class action lawsuits, QSFs have since extended to the broad breadth of legal conflicts such as single events, single claimant personal injury claims, and contract breaches.

To establish a QSF, specific requirements must be met:

- Be approved by a “governmental authority” defined by 26 C.F.R. §1.468B-1(c)

- Be under the continuing jurisdiction of the approving governmental authority

- Be set up to resolve one or more legal claims

- Qualify as a trust under applicable state law if established as a trust

PRO TIP: Online QSF platforms like QSF 360 can fully establish a QSF in as little as one business day.

Advantages of Using QSFs for Post-Settlement Resolution

Qualified Settlement Funds offer numerous advantages for all parties involved in post-settlement dispute resolution. By establishing a QSF, defendants can claim immediate tax deductions and extricate themselves from ongoing litigation. At the same time, plaintiffs gain tax deferral, which provides them valuable time to make informed decisions regarding the allocation of settlement funds, aiding in the negotiation of competing claims and liens, and implementation of financial and tax planning strategies.

Avoiding Conflicts of Interest and Ensuring Fair Distribution

Conflicts arise when plaintiffs and their family members are suing each other, and sometimes even when the lawyers get into the act by suing one another or their clients over the allocation of the settlement. Qualified Settlement Funds offer a way to handle these disputes by allowing tax-deferred time to resolve the conflict and preserving the core settlement. The QSF administrator administers the distribution depending on each case’s details and implements the court’s final instructions.

Conclusion

The use of QSFs has transformed how lawyers and their clients navigate the realm of post-settlement disputes and allocation affairs. By offering a streamlined approach to settlement fund management, addressing liens and conflicts, and facilitating settlements, QSFs bring numerous advantages to all parties involved.

By staying up to date, collaborating with experienced QSF professionals, and adapting to the requirements of each case, attorneys and plaintiffs can harness the full potential of QSFs and secure optimal outcomes in the post-settlement stage.

.png)

Eastern Point Unveils Comprehensive Guide on Taxable and Tax-Free Settlements

Eastern Point is proud to announce the release of its latest publication, Unveiling the Complex World of Taxable and Tax-Free Settlements.

FOR IMMEDIATE RELEASE

[5/17/2024] — Eastern Point is proud to announce the release of its latest publication, Unveiling the Complex World of Taxable and Tax-Free Settlements. This comprehensive guide delves into the intricate workings of taxable and non-taxable settlements, offering invaluable insights into compensatory damages, punitive damages, and the tax treatment of various settlement types.

Ms. Rachel McCrocklin, Eastern Point’s Chief Trust Officer, commented, “The guide provides a detailed understanding of the pivotal role of IRS Section 104 and the taxability of various settlement types. Our goal is to equip readers with the knowledge to make informed decisions and minimize potential tax liabilities.”

The guide explores strategic methods to minimize tax obligations on settlements, including leveraging structured settlement annuities, Plaintiff Recovery Trusts, and proper allocation in settlement agreements. It is an essential resource for individuals and businesses navigating the complex landscape of settlement taxation.

Arm yourself with knowledge, make informed decisions, and minimize potential tax liabilities with Eastern Point's newest guide.

For more information on Unveiling the Complex World of Taxable and Tax-Free Settlements, please visit https://www.easternpointtrust.com/articles/unveiling-tax-free-settlements-what-you-need-to-know or contact 855-222-7513.

CTRO

PRESS Contact

www.EasternPointTrust.com

info@easternpointtrust.com

Phone: 855-222-7513

Unveiling Tax-Free Settlements: What You Need to Know

What Types of Legal Settlements are Not Taxable?

Settlements and their tax implications can often seem complex for individuals and businesses. It’s essential to grasp the nuances involving taxation of settlements to make informed decisions and reduce tax burdens.

This article dives into the details of taxation of settlements, offering insights into compensatory damages and punitive damages, as well as how different settlement types, like whistleblower settlements, are treated for tax purposes. This article also discusses strategies for minimizing tax responsibilities on settlements and answers common questions such as how to report settlement funds to the IRS and determining the portion of a taxable settlement.

Differentiating Taxable Income From Taxable Settlements

Per Section 61 of the Internal Revenue Code (IRC), all income is generally taxable unless explicitly exempted by another section of the IRC. The taxation of settlements hinges on the nature of the claim and the damages awarded.

Understanding Settlement Taxation

The taxability of settlements is contingent upon “the origin of the claim,” meaning the cause of action that led to the settlement award. Here’s a breakdown illustrating how typical settlements are taxed:

When determining the taxability of a settlement, consider these key factors:

- What was the settlement intended to replace?

- Is there a specific exemption in the tax code that applies?

The Role of IRC Section 104 – Physical Injury

IRC Section 104 excludes certain settlements and awards from taxable income. Specifically, §104(a)(2) of the IRC allows taxpayers to exclude from gross income “the amount of any damages (other than punitive damages) received on account of personal physical injuries or physical sickness.”

However, there are some important nuances to keep in mind:

- The injury must be physical in nature.

- Punitive damages are generally taxable, even if they relate to a physical injury, with a narrow exception for certain wrongful death cases.

Before 1996, Section 104(a)(2) did not have the “physical” requirement. The Small Business Job Protection Act of 1996 changed the code to restrict exclusions for injuries and sickness.

PRO TIP: Emotional distress alone does not qualify for the exclusion under §104(a)(2) unless it originates from a physical injury or sickness.

PRO TIP: Attorney fees that come with damages cannot be deducted by the plaintiff. So, the plaintiff will need to pay taxes on the amount of the award. (Refer to the discussion on strategies in the Plaintiff Recovery Trust to avoid this “double tax” situation.)

PRO TIP: Taxpayers must show that their settlement qualifies for exclusion under Section 104(a)(2). The IRS will review the language in the settlement agreement and legal claims to determine tax treatment. Using precise language in both settlement agreements and court orders can strengthen a taxpayer’s case.

Common Nontaxable Settlements

Settlements stemming from physical injury or illness are generally deemed nontaxable under Internal Revenue Code (IRC) Section 104 (a)(2). These settlements compensate individuals for injuries or sickness. Let’s look at some examples.

Personal Injury Settlements

Settlements received for personal physical injuries are typically nontaxable, including compensation for:

- Dog bites and attacks

- Motor vehicle accidents resulting in physical injury

- Medical malpractice suits based on physical illness or sickness

- Premises liability cases where injury results from property neglect

- Workplace and construction injuries

- Product liability, such as defective medications causing severe harm

The critical factor is that the settlement involves physical injury or sickness. Emotional distress damages originating from a physical injury are also nontaxable.

Medical Expense Reimbursements

When a settlement includes reimbursement for expenses related to the injury, the part of the settlement designated for those expenses is usually not taxable unless those medical expenses were previously deducted by the plaintiff. If, in a prior tax year, the medical expenses were deducted and a tax benefit was provided, then that portion of the settlement may be considered income.

Wrongful Death Settlements

Similarly, settlements for death cases are generally treated as nontaxable since they are handled similarly to injury settlements from a tax perspective. These settlements compensate the surviving family members for reasons including the loss of support, the pain and suffering experienced by the deceased, medical and funeral expenses, and the loss of potential inheritance. However, there are exceptions to consider. Punitive damages in cases of wrongful death are typically subject to taxation. Moreover, any part of the settlement that reimburses expenses previously deducted by the plaintiff may be regarded as income up to the extent of any tax benefits received.

PRO TIP: Contingent attorney fees associated with punitive damages are not deductible to the plaintiff. Accordingly, the plaintiff must pay taxes on the entire amount of the punitive award. (Plaintiff recovery Trust discussion below for strategies to eliminate this “double tax”)

Carefully review the specific circumstances of each settlement to determine the appropriate tax treatment. Consulting with a tax professional can help ensure compliance with IRS regulations.

Common Types of Taxable Settlements

Some settlements are not subject to taxes; however, some require taxation. Let’s delve into some examples of these settlements in detail.

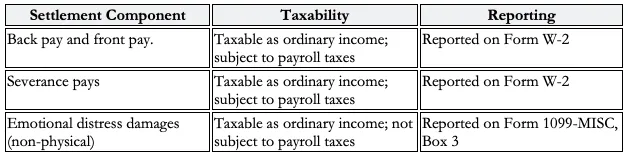

Employment Disputes and Lost Wages

Compensation received for lost wages, back pay, front pay, or severance pay is considered income and is subject to taxes, including Social Security and Medicare taxes (FICA) withholding. Here’s a breakdown of how these settlements are taxed:

It’s crucial to understand that even if some of the settlement pertains to distress damages stemming from an employment dispute, those damages remain taxable unless they result from an injury or illness.

Punitive Damages

Punitive damages are always taxable regardless of the case’s nature. These damages aim to penalize the defendant for their misconduct and do not serve as compensation for the plaintiff’s losses. Punitive damages are categorized as “Income” on Form 1099 MISC. Are taxed as ordinary income rates.

- Punitive damages are taxable even if the underlying compensatory damages are tax-free, such as in a personal physical injury case.

- The plaintiff must pay taxes on the entire gross amount of punitive damages awarded, including the portion paid to their attorney as a contingency fee.

- Punitive damages are not subject to payroll taxes, as they are not considered wages or compensation.

PRO TIP: Contingent attorney fees associated with punitive damages are not deductible to the plaintiff. Accordingly, the plaintiff must pay taxes on the entire amount of the punitive award. (Plaintiff recovery Trust discussion below for strategies to eliminate this “double tax”)

Emotional Distress Without Physical Injury

When it comes to distress without injury, payments received for mental anguish or emotional distress are usually subject to taxation unless they stem from a personal physical injury or illness. These payments may be tax-free if an injury causes emotional distress. However, these payments become taxable if emotional distress leads to symptoms like headaches or stomachaches.

Let’s consider some examples:

- Emotional distress damages arising from a non-physical injury (e.g., discrimination, defamation) are taxable.

- Emotional distress damages that cause physical symptoms but do not originate from a physical injury are taxable.

- Emotional distress damages that originate from a physical injury or sickness may be tax-free.

When receiving a settlement for emotional distress, it’s crucial to work with a tax professional to determine the appropriate tax treatment based on the specific circumstances of your case.

Whistleblower Taxation

There is no tax exemption exception for False Claims Act whistleblower awards. As such, whistleblowers must pay income taxes on their rewards at the ordinary income tax rates. As such, it remains wise to seek competent advice, as tax questions regarding whistleblower rewards are complex.

PRO TIP: Federal and state income tax burdens apply to qui tam rewards like any other form of ordinary income.

Strategies to Minimize Tax Obligations on Settlements

For those seeking to minimize settlement tax obligations, there are strategies available to reduce the taxes and maximize the recovery for plaintiffs. Utilizing settlement annuities, the Plaintiff Recovery Trust, and proper allocation in settlement agreements can help individuals reduce their tax burden and secure their future.

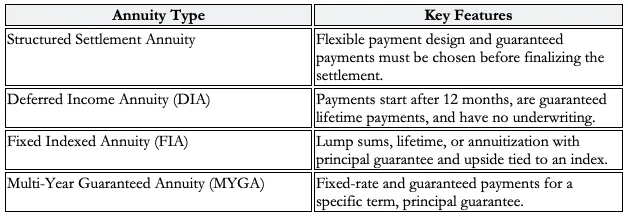

Structured Settlement Annuities

Structured settlement annuities provide a tax option for recipients of settlements by spreading out the settlement payments over several years instead of receiving a lump sum. This approach helps lower the tax rate. It offers benefits such as tax deferral, guaranteed growth of funds within the annuity, and enhanced financial stability. Regular payments can help secure your future and prevent spending decisions. Different types of annuities offer diverse features:

Plaintiff Recovery Trusts

Moreover, Plaintiff Recovery Trusts (PRTs) are tools to avoid taxation for plaintiffs receiving settlements that include attorney fees. By transferring the litigation interest to the trust, plaintiffs only pay taxes on their recovery as beneficiaries, increasing after-tax earnings by 30 to 70%.

PRTs offer additional benefits:

- Increased Premiums: PRTs can increase available structure premiums by 30% in a typical case.

- Simplified Fee Deferral: PRTs eliminate the need to match payment schedules for lawyers’ deferred fees.

- Asset Protection: PRTs can offer increased safeguarding, against creditors by operating as an entity.

Proper Allocation in Settlement Agreements

The tax implications of settlements hinge on the source and nature of the claims involved. By distributing settlement funds in the agreement, plaintiffs can optimize the portion of their recovery exempt from taxes.

- Identify Tax-Free Damages: Allocate funds to claims for personal physical injuries or physical sickness, which are generally tax-exempt under IRC Section 104(a)(2).

- Separate Punitive Damages: Allocate punitive damages separately, as they are always taxable, regardless of the underlying claim.

- Negotiate at Arm’s Length: Ensure allocations result from adversarial, good-faith negotiations to withstand IRS scrutiny.

By strategically employing structured settlement annuities, plaintiff recovery trusts, and proper allocation in settlement agreements, plaintiffs can significantly minimize their tax obligations and maximize their net recovery, providing long-term financial security and peace of mind.

Conclusion

The tax consequences associated with settlements can be complex and diverse, underscoring the importance for individuals and organizations to grasp the intricacies of taxable versus taxable settlements.

Understanding the basics of damages, punitive damages, and how settlements are taxed can help readers make informed decisions to lower their tax burden. Utilizing methods like settlement annuities, plaintiff recovery trusts, and careful allocation in settlement agreements can cut down on taxes. Increase the final amount received. It’s advisable to seek guidance from tax experts and lawyers to handle the intricacies of settlement taxation in line with IRS rules.

Maximizing A Court Award - Strategic Tax Planning for Post-Judgment Interest

Introduction

You prevailed and won the case, and the award includes post-judgment interest – now, taxes are due on the interest.

Unfortunately, many people are taken aback when they find out that post-judgment interest is always taxable in cases involving injuries.

Knowing how this interest is taxed and being ready for it is often overlooked when planning for matters. This discussion focuses on the tax implications of post-judgment interest in physical injury cases and ways to reduce its tax burden.

Is Post-judgment Interest Material?

The notion that post-judgment interest is not material can be fatally flawed. As the appeals process can drag on for years, it is not at all unusual for post-judgment interest to be significant. In today’s courts, cases with millions of dollars in post-judgment interest are not rare.

Pro-Tip: As time passes, tax planning options diminish. Therefore, the time to start planning to mitigate post-judgment interest taxation is before the case is final – the earlier, the better.

Understanding the Taxation of Awards

- Generally, compensation for physical injuries or sickness is non-taxable, including the associated medical bills and lost wages.

- On the other hand, damages for non-physical injuries (such as emotional distress), defamation, and humiliation are ordinarily taxable.

Pro Tip: Taxation of Post Judgement Interest Still Applies Under IRC Section 104. Damages received for injuries or sickness are not taxable gross income under §104(a)(2). However, it’s important to note that this tax exemption does not extend to damages or post-judgment interest. As a result, punitive damages and post-judgment interest are always subject to taxation, irrespective of the type of injury.

Pro Tip: Legal Fees and Deductions.

The 2017 tax law eliminated the deduction for attorney fees linked to awards or settlements. As a result, individuals filing lawsuits now need to include the entire amount of their taxable recoveries as taxable gross income without being able to deduct any legal fees. For more details, click Double Tax.

Tax Planning Strategies for Recipients of Post-Judgment Interest

Utilizing Plaintiff Recovery Trusts

The Plaintiff Recovery Trust (PRT) allows plaintiffs to reduce the tax implications of taxable awards (including post-judgment interest). This specialized trust enables plaintiffs to skip paying taxes on the attorney fee portion of the judgment or settlement, including those linked to judgment interest. As a result, the PRT offers the advantage of helping plaintiffs retain a greater after-tax percentage of the award.

Structured Settlement Annuities and Tax Benefits

Structured settlement annuities, while beneficial, offer less effective strategic tools for plaintiffs to reduce the taxation on post-judgment interest.

Conclusion

Navigating the complexities of post-judgment interest and its tax implications is often an overlooked planning element. The Plaintiff Recovery Trust typically will offer the best taxation outcomes on post-judgment interest awards, and by preplanning to utilize the PRT, recipients can significantly enhance their economic results.

As such, when the possibility exists of court awards with post-judgment interest, one should proactively engage in tax planning strategies EARLY – waiting until after the final award or the appeal is often too late.

You Have Needs,

We Have Expertise

Discover trust and settlement solutions you won’t find anywhere else – thoughtfully designed to protect assets, simplify processes, and deliver peace of mind.

Expert guidance, every step of the way.

.svg)